In October 2024, the Chancellor confirmed in the Autumn Budget that the government will abolish the tax rules for non-UK domiciled individuals, replacing them with a residence-based regime from 6 April 2025.

The new regime moves away from the concept of domicile to the more direct determination of residence to define an individual’s UK tax status. It is therefore essential that individuals understand and track their residence status in order to plan for their personal taxation in the UK.

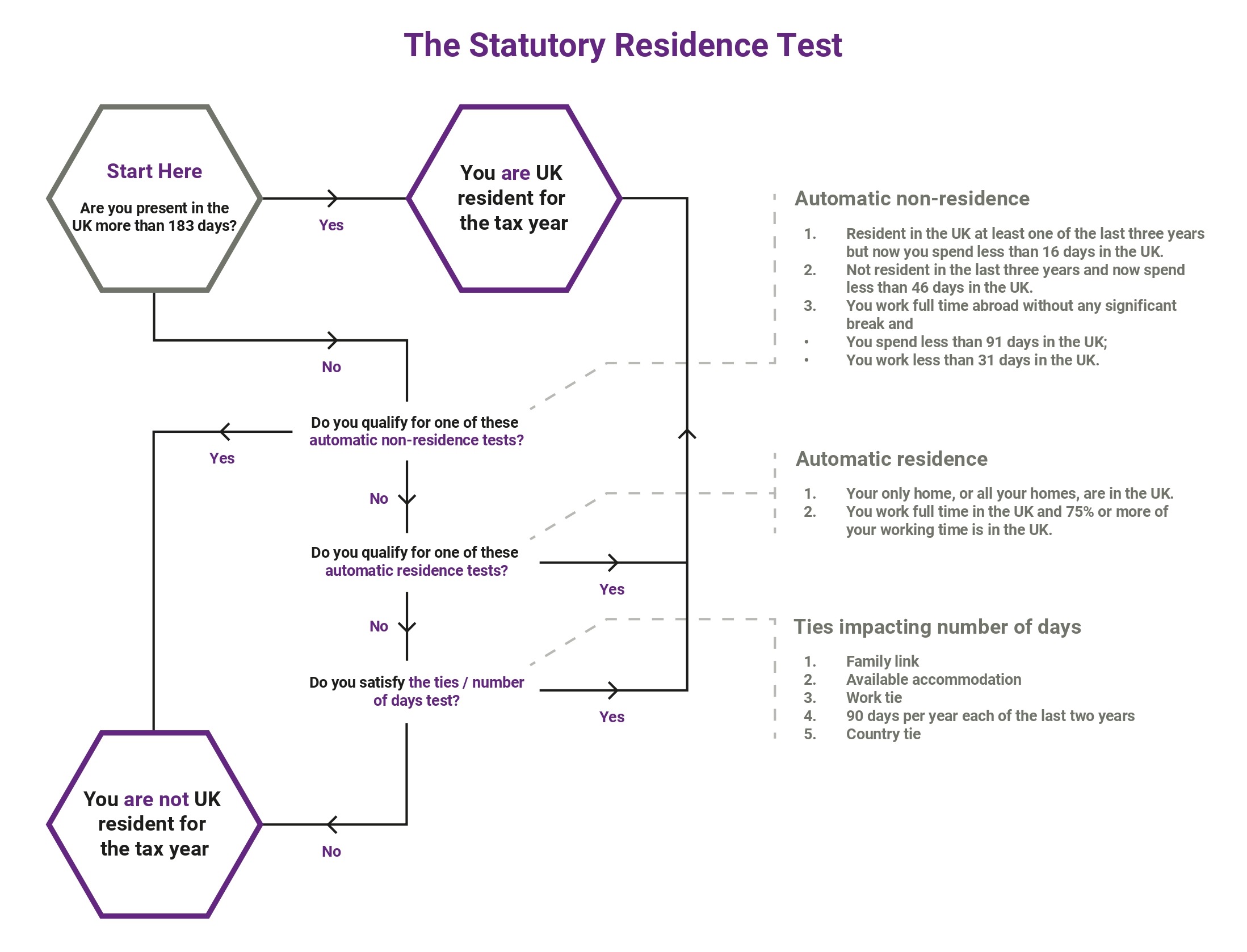

The Statutory Residence Test (SRT), which determines an individual’s position as a tax resident in the UK, means that in some circumstances, an individual may only need to be present in the UK for 16 days before becoming tax resident. In other circumstances, an individuals could be present in the UK for 182 days, without being tax resident.

The SRT offers a relatively methodical route to assess residence status for any given tax year. Each tax year is examined separately, as is each individual, so residence in the UK may be achieved in one year but not the next, or vice versa. Despite the relative certainty, with over 200 pages of notes accompanying the SRT rules, it remains crucial that individuals seek specific advice on their own personal circumstances.

The SRT consists of a number of stages and a variety of rules that, in combination, determine whether an individual is UK resident or non-UK resident for tax purposes in a particular fiscal year. To determine residential status, an individual progresses through the following three ‘tests,’ moving onto the next stage only if required:

Click on the image for a closer look

It is the ‘sufficient ties’ test which considers the individual’s connections with the UK, together with their status as a leaver or a new arrival, that determines how many days would trigger tax residence.

Our Introduction to the Statutory Residence Test guide can help you understand the considerations that determine UK tax residence. However, we suggest that if there is any uncertainty, suitable professional advice should be taken.

The international team at Partners Wealth Management has been dealing with the concepts of domicile, remittance, mixed funds, and participated in consultations about the new regime with HMRC. We also have worked with a vast number of lawyers and accountants, along with other professional advisers in order to advise our clients about their family wealth.

We are used to working with cross border and complex situations utilising strong methodology, vast professional network and in-depth knowledge of available strategies. Please contact any of our International team for a no-obligation introductory meeting to discuss how we can help you with your international financial considerations.

The concept of residence will be a key consideration for any individual moving to or from the UK, as it has a fundamental impact on a person’s potential tax liability. Our guide considers some of the key questions we have been asked by clients in this area.

On 6 April 2025 the new Foreign Income and Gains (FIG) Regime was introduced, replacing the previous system based on domicile. Our guide outlines the new rules applicable to both existing and new UK residents.

Every year a significant number of UK nationals who have expatriated abroad return to the UK. This will be for many different reasons but one thing everyone has in common is, just as you will have considered your financial position before you left, you need to do so again before you return.

For further information on how we can help you build and protect your wealth, please contact us.